The Disney Inflection: Technical Clouds, CEO Succession, and the Road to FY26

$26B in revenue and a new CEO: Is the Disney turnaround real? A Look at what the charts are telling us

Table of Contents

Big News at Disney

Disney had a big leadership update on Feb. 3 as the board picked Josh D’Amaro as the next CEO, replacing Robert Iger.

The takeaway for investors is simple: the company now has a clearer succession plan, but the spotlight shifts to execution—especially whether an executive best known for parks and “Experiences” can keep momentum in streaming, manage the studio slate, and navigate a changing sports media landscape.

Looking at Disney’s most recent quarter (fiscal 1Q26, ended Dec. 27, 2025), the company showed progress in streaming, but a mixed picture elsewhere.

Revenue rose to $26.0B (+5% year over year) — sales were up in all three major segments:

Entertainment (+7%)

Sports (+1%)

Experiences (+6%)

However, operating profit fell in Entertainment and Sports.

Meaning, growth is there, but profitability isn’t rising evenly across Disney’s portfolio.

Streaming was the bright spot (thanks, Bluey). Management said the subscription streaming business generated $450M in operating profit (up 72% year over year) and guided to about $500M next quarter, while reiterating a longer-term aim of a 10% streaming operating margin for FY26.

Source: Wikipedia

That’s why the market continues to focus on whether Disney can keep improving streaming economics without sacrificing subscriber stability or content quality.

Strategically, Disney is leaning into two areas.

First, it’s upgrading its product and advertising capabilities—including AI-enabled ad tools—and it disclosed a licensing agreement with OpenAI tied to Sora content for Disney+.

Second, the company is pushing harder on sports sold directly to consumers through ESPN, including a path toward a broader DTC product (often referenced as “ESPN Unlimited”) and ongoing rights/portfolio moves (including a Major League Baseball agreement and a transaction involving NFL Network / NFL RedZone).

Sector Outlook

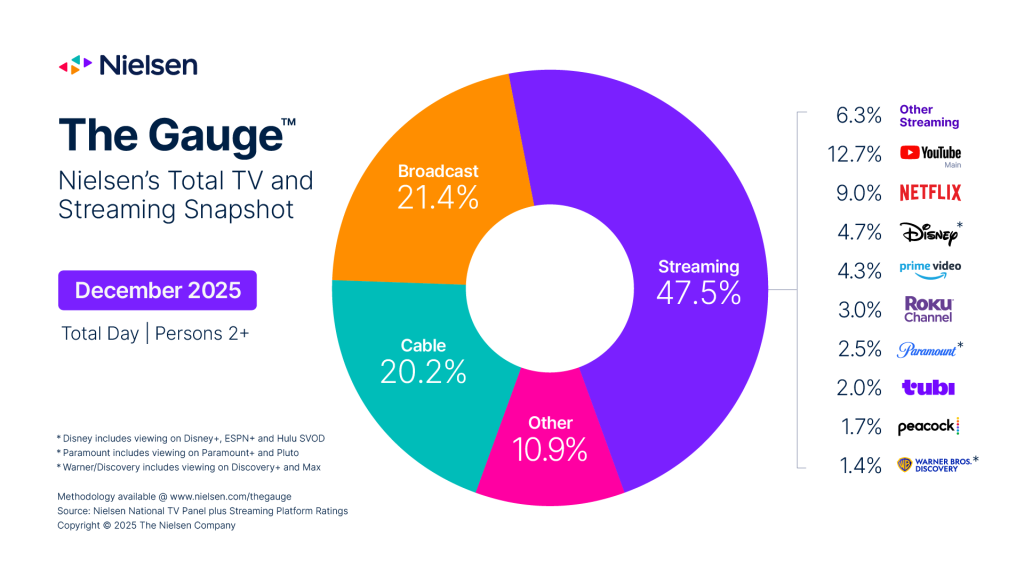

The media landscape is still shifting quickly as streaming continues to take share from traditional TV (that thing your parents still watch).

Nielsen reported that streaming reached a record 47.5% of total TV viewing in December 2025.

Source: Nielsen

That trend keeps long-term pressure on the old pay-TV bundle, which matters for Disney because it weighs on the economics of linear networks (fewer subscribers, harder ad comparisons, and less stable affiliate fees).

At the same time, streaming is no longer a “growth at any cost” story.

Industry forecasts (including work often cited from AlixPartners and Ampere Analysis) still expect continued growth in online video, but competition for both viewing time and ad budgets remains intense—especially with more services offering lower-priced ad-supported options.

For scaled players like Disney, the opportunity is to win on brands, franchises, and sports while improving ad monetization and reducing churn through smarter bundling.

Experiences (theme parks, cruises, consumer products) are still a strong pillar, but it’s not immune to the current economic cycle.

Demand tends to hold up better for higher-income consumers, but international travel trends can swing results—especially the mix of domestic vs. international visitors and what that means for pricing and per-guest spend.

In this backdrop, the main debate is less about pure attendance and more about whether Disney can protect pricing power and deliver a great on-property experience while managing costs.

What Do the Charts Say

Disney stock (DIS) is down nearly 50% since its March 2021 peak. So, is it time to buy? Let’s see what the charts show.

Zooming in, Disney has been stuck in a longer-term sideways trend since 2022:

If the sideways trend continues, there is a risk of a further 20%+ decline in Disney’s stock price.

What is the likelihood of this happening? Let’s examine two concepts:

The “Cloud” Model

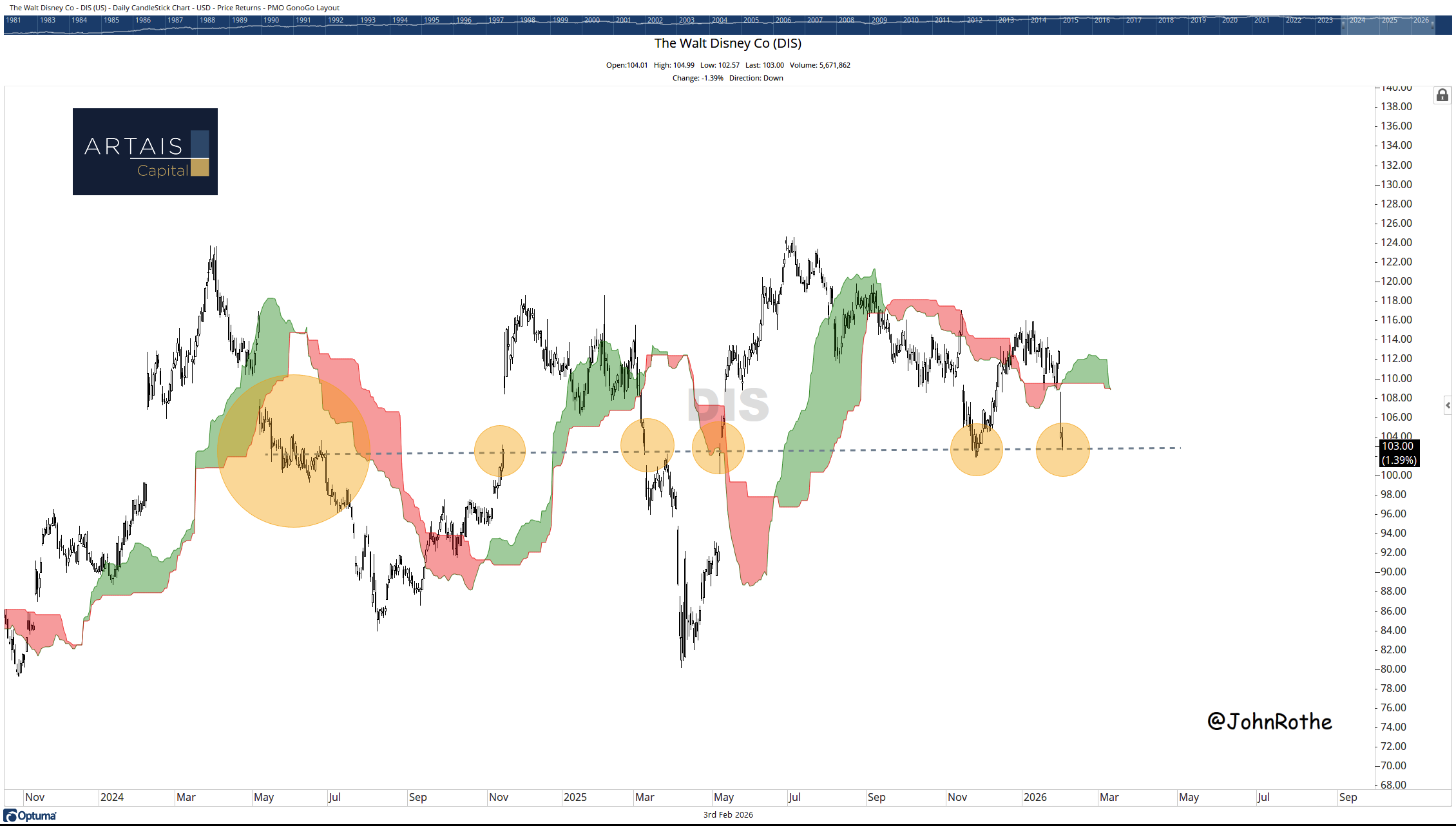

One of the tools I use to help identify market trends is the Cloud model. The “Cloud”, which is represented by the green and red shaded areas, can help us visualize the current trend of the stock and is based on the Ichimoku Cloud.

It allows us to see if the trend is rising, falling, or moving sideways. The Cloud model also provides us with levels of support and resistance.

The proprietary model at ARTAIS Capital uses the cloud as a way of filtering stock selection. Typically, we only focus on stocks that are trading above the cloud. (Those stocks are then narrowed down with additional tools, analysis, and risk management.)

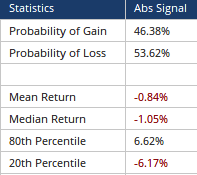

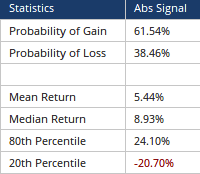

Going back to 2000, every time Disney’s stock has broken below the cloud, the probability of gain over the next 90 days falls below 50%.

For my fellow finance nerds who are familiar with Optimal f and Risk of Ruin, those results are pretty bad.

Source: OPTUMA

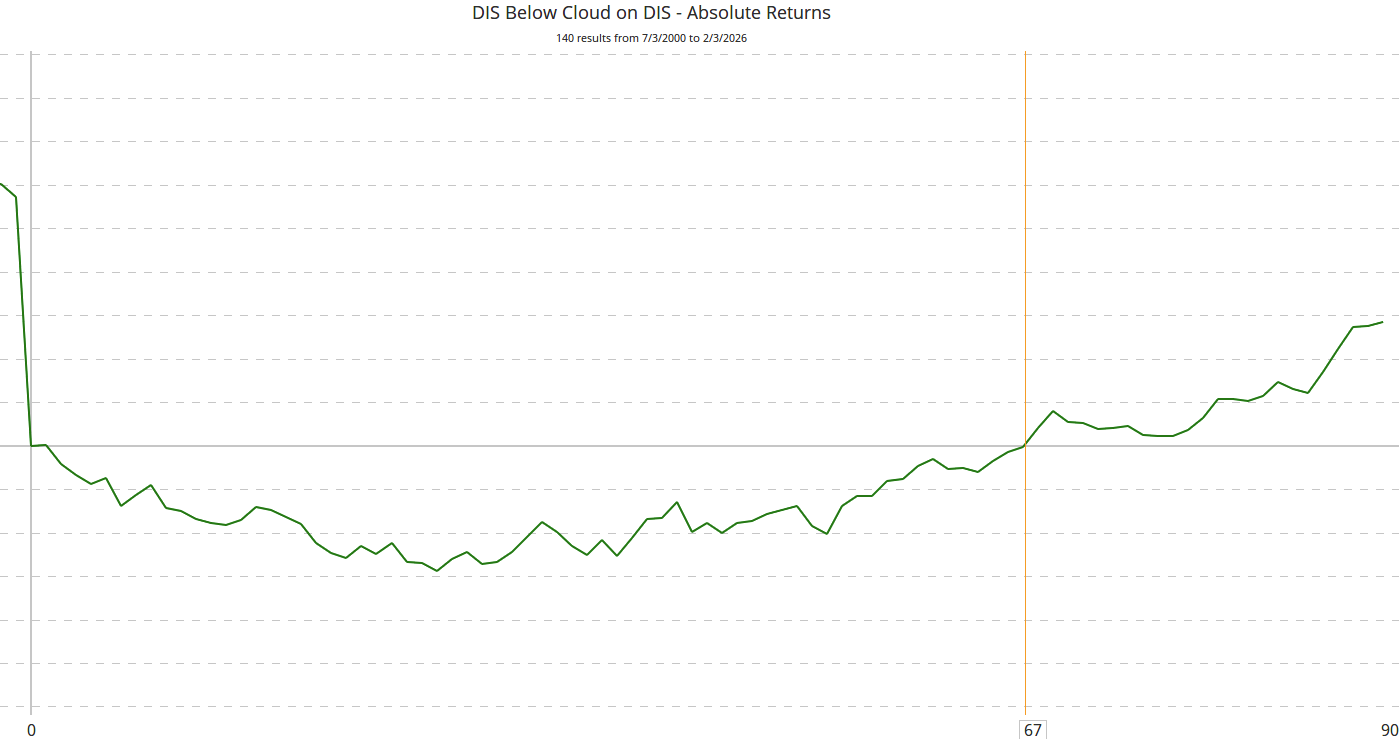

What is interesting in studying the data is that during the 140 times Disney has crossed below the cloud since 2000, the stock reverses and begins to show a positive gain around day 67.

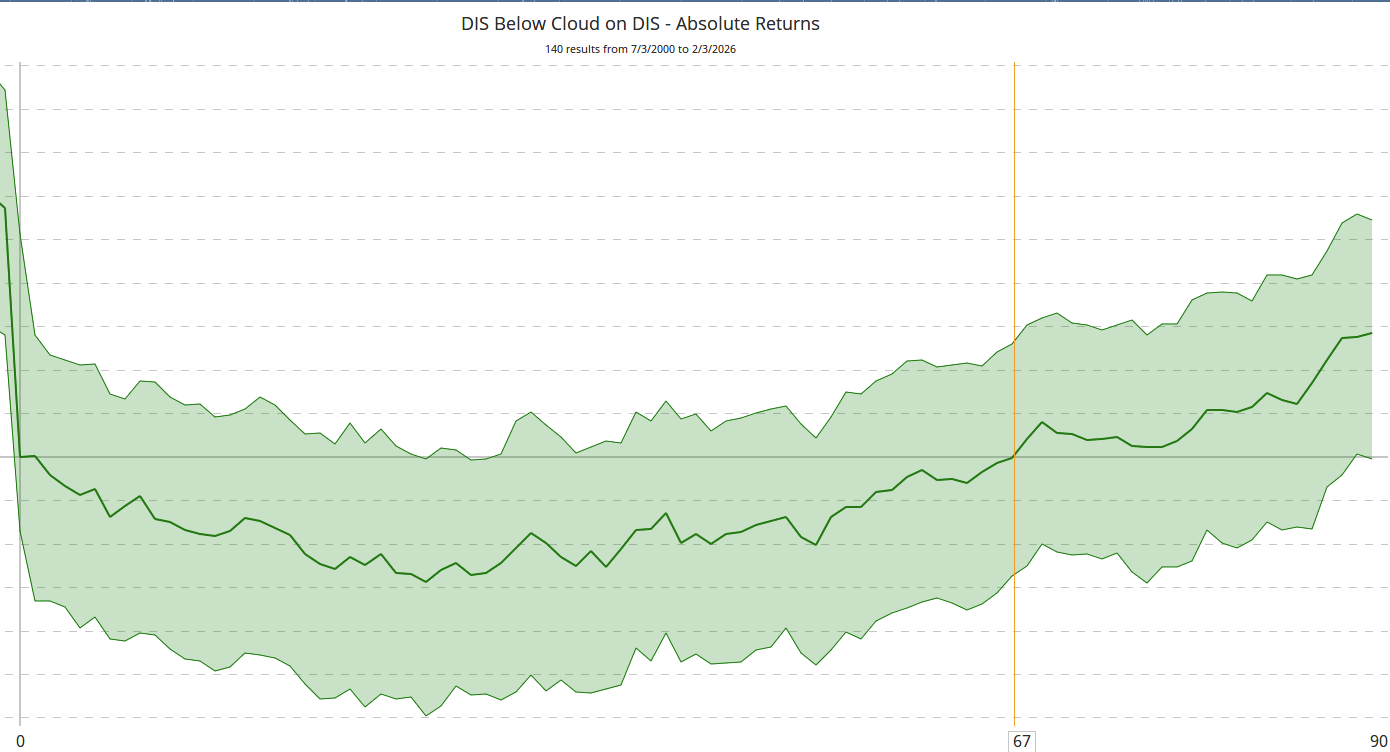

Of note, the above image is the average. The range of this data can vary tremendously, potentially placing the switch in trend to 90+ days:

2) Finding Price Support

Disney’s stock is currently (as of 2/3/2026) trading near an inflection point - an area which investors have viewed as a buying opportunity.

Before anyone gets too excited, this has also been an area of past breakdowns.

Why should we pay attention to these support/resistance levels? It tells us how large institutional players are viewing the company.

If they fail to come in to buy at these key levels, it is an indication that these large investors don’t find value at the current level (whereas they found value at this level previously).

Which is why we typically see quick and large drops in a stock’s price when support is broken.

While more aggressive traders might be tempted to “test the water” at these levels, I prefer to wait for the price to cross above the cloud.

Using the same parameters from above, after Disney crosses above the cloud, the results tend to be more favorable:

Potential Catalysts

The next couple of months have several “headline” events that could move sentiment.

In my opinion, the CEO transition, which is scheduled for March 18, 2026, is likely to be a key positive or negative moment for the stock, as Wall Street digests a newly refreshed strategic messaging and a clearer sense of priorities under new leadership.

This is where we will see how much confidence Wall Street has in incoming CEO Josh D’Amaro.

Additionally, Disney highlighted the planned March 2026 opening of World of Frozen at Disneyland Paris, which investors may use to gauge international park demand.

Disney Cruise Line is another swing factor: new ship launches can temporarily pressure margins due to ramp costs (ramp costs refer to the high, upfront expenses incurred while preparing a new vessel for service and operating it during its initial, non-peak phase), even if they improve longer-term growth.

Disney noted that the new ship, Disney Adventure, is scheduled for a March 10 maiden voyage; early booking strength and onboard spending will matter for the narrative.

Finally, the next earnings date for fiscal 2Q26 hasn’t been formally confirmed on Disney’s investor relations calendar, but I would expect it to be held early to mid-May 2026.

Investors will be focused on a few core questions:

Are streaming profits still improving?

Is sports DTC making tangible progress?

And are parks and cruises holding up on pricing and spending per guest?

Conclusion

Short-term traders may test current support levels, hoping that large institutional funds still see value at the current levels.

I wouldn’t be surprised to see consolidation in price, including a tighter trading range, as investors wait to hear from incoming CEO Josh D’Amaro as the transition period gets closer and closer.